I recently attended MATCH-UP 2024 at Oxford, where I saw Julius Goedde present the paper “Pricing in markets without money: Theory and evidence from home exchanges”. I found it quite interesting! The paper considers platforms that enable home exchange – examples include Trade to Travel, People Like Us, and Home Exchange.

The idea behind all of these sites is, you let strangers stay in your home, and in turn you can visit somewhere else in the world for free! Originally, most of these marketplaces sought simultaneous pairwise exchanges. That is, you find someone else on the platform, and swap homes for the week. As you can imagine, this can be difficult: if I want to visit Costa Rica in January, what’s the chance that someone from Costa Rica wants to visit Saint Paul at the same time? (Given average January temperatures, not so good.) Things become slightly easier if exchanges are allowed to be non-simultaneous. That is, I stay in a home in Costa Rica in January, and in return owe the owners of that home a future visit to Saint Paul at a mutually agreeable time (for example, July, when weather in Minnesota tends to be nicer). Of course, for this to work, I need to figure out where I will live when they visit!

Credit (Fake Money) Systems on Home Exchange Platforms

What if I want to visit Costa Rica, but my hosts in Costa Rica don’t want to visit Minnesota at all? Well, maybe they want to visit Los Angeles, and someone in Los Angeles wants to visit Vancouver, and the person in Vancouver wants to visit Minnesota. But arranging a four-way swap seems totally impractical, so instead these platforms have created token (fake money) systems. I stay with the family in Costa Rica, and pay them credits which can be used to pay for future stays on the platform. To earn those credits, I have to host myself. Voila! These credits serve as a medium that enables exchange.

Now, there’s something important to recognize. Not all homes offered on these platforms are equally nice. They have different they have different sizes, amenities, and locations. And yet, some platforms require all homes to cost the same number of credits. That is, each time someone hosts, they earn enough credit for a stay somewhere else. (For example, People Like Us calls these credits “globes” and writes “A Globe is worth one stay at another member’s place.”)

This seems strange. If the “cost” of a stay (in credits) does not depend on how nice the home is, won’t everyone just stay in the nicest home they can find? Nice homes will get a flood of requests, while not-so-nice ones might not get any. This could prevent people with not-so-nice homes from obtaining any credits at all! To an economist, there is an obvious way to address these concerns: allows prices to adjust freely, so that less desirable homes cost fewer credits to book. In fact, many platforms (such as Trade to Travel) do something like this. Are platforms that fix prices making a big mistake, or could they be on to something?

This paper argues the latter, and provides a very nice intuition. Each person can only go on so many vacations. If I have a very nice home that earns me a lot of credits each time it is booked, then hosting once or twice might give me enough credits for the entire year. Because hosting is a hassle, I won’t host any more than I need to. If the platform requires that I host once for every trip I want to do, I might choose to host more often. Thus, constraining prices could (somewhat surprisingly) increase the supply of high-quality homes on the platform.

Another way to think about this is that requiring prices to be equal essentially makes people with nice homes “poorer” than they would be with market-clearing prices. As a result, they have to work harder (host more visitors) in order to be able to afford the trips they want to make.

The paper includes both a stylized model and an empirical component using proprietary data from a home exchange platform. I’m not an empiricist, so I will mostly focus on the theoretical model.

Model

In their model, users arrive and depart over time. There are several key assumptions:

- Over the course of their lifetime, each person may host at most twice and may visit at most two homes. (Think of this as arising from having only two weeks of vacation – during which you can travel and/or let someone else live in your home – rather than an explicit constraint imposed by the platform.)

- Visiting others’ homes offers positive utility, but hosting is costly: people won’t do it unless they get something in return.

- Each visit costs virtual currency, which can only be earned by hosting. For each person, total virtual currency earned by hosting must at least equal virtual currency spent on visits. (Extra unspent virtual currency is worthless.)

- There are two types of homes, “low value” (L) and “high value” (H), in equal quantity. Everyone agrees that \(H\) homes are preferable to \(L\) homes.

Payoffs are as follows. Each time an agent of type \(A \in \{L, H\}\) visits a home of type \(B \in \{L, H\}\), the visitor incurs a reward of \(V_B^A\) and the host incurs a cost of \(C\) (which is the same for both types of homes, though this assumption could easily be relaxed). To compensate the host, the visitor pays \(p_B\) in virtual currency to the host, which the host can spend on future trips. Importantly, this virtual currency has no use other than booking trips.

Analysis

The goal of the paper is to compare the outcome under market-clearing prices (where \(p_H\) and \(p_L\) are set to ensure that supply equals demand) to outcomes when the platform requires that prices for all homes are equal.

First, consider market-clearing prices. Because everyone prefers \(H\) homes, prices for these homes will necessarily be lower than those for \(L\) homes. There are only two types of equilibria that can arise:

- Separating equilibrium. The two markets function independently: high types host and visit other high types, and likewise for low types. (Everyone hosts twice and is a guest twice.)

- Trading equilibrium. The price for an \(H\) home is twice the price for an \(L\) home. Low types host twice, and use the proceeds to get a single stay at an \(H\) home. High types host once, and use the proceeds to pay for two stays at \(L\) homes.

Note that in this second type of equilibrium, there are \(H\) homes that are not being visited as frequently as they could be. The reason is that the owners are satiated: they are able to “afford” two trips already, so see little benefit to hosting more often. (They could choose to host twice in order to upgrade their accommodations from \(L\) to \(H\), but the cost of hosting is large enough that they prefer not to do this.)

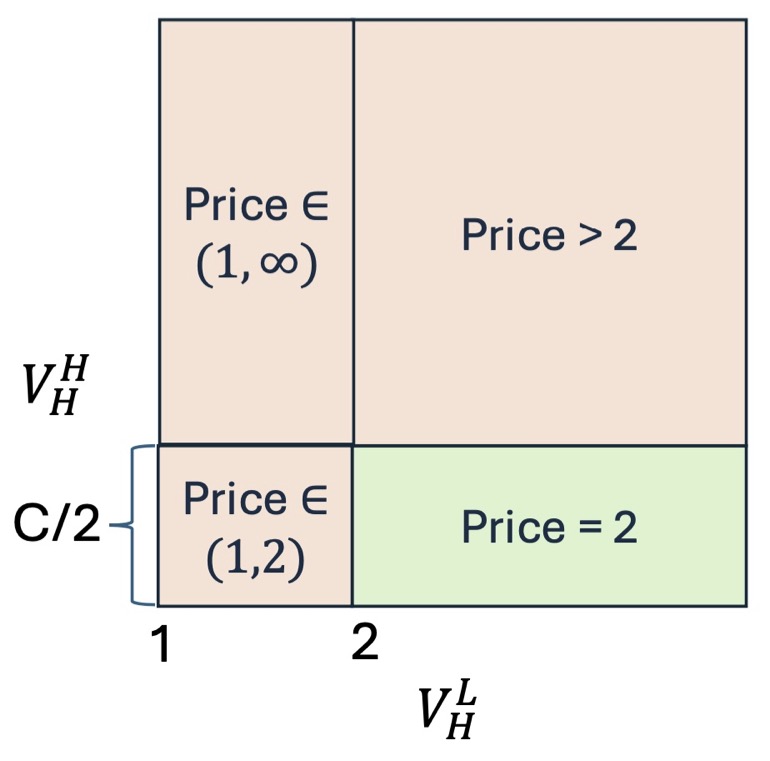

Because multiplying utilities by a scalar has no effect on agent decisions, we can assume without loss of generality that \(V_L^H = V_L^L = 1\). This leaves three parameters: \(V_H^H, V_H^L\) (both greater than \(1\)), and \(C\) (assumed to be less than \(1\)). The following figure shows when each equilibrium arises, and what conditions the equilibrium “price” \(p_H/p_L\) must satisfy.

Figure 1: In the red region, high and low types essentially form separate markets: people with \(H\) homes host and visit others with \(H\) homes, and likewise for those with \(L\) homes. In the green region, those with \(H\) homes choose to rent only once, and visit two \(L\) homes. “Price” refers to the ratio of the price of an \(H\) home to the price of an \(L\) home.

For a trading equilibrium to occur, two conditions must be met. First, low types must prefer a single stay in an \(H\) home to two stays in an \(L\) home (\(V_H^L > 2\)). Second, high types must find hosting inconvenient enough that they prefer hosting once and staying in two \(L\) homes to upgrading those stays by hosting a second time (after some algebra, this is true if \(V_H^H < 1 + C/2\)).

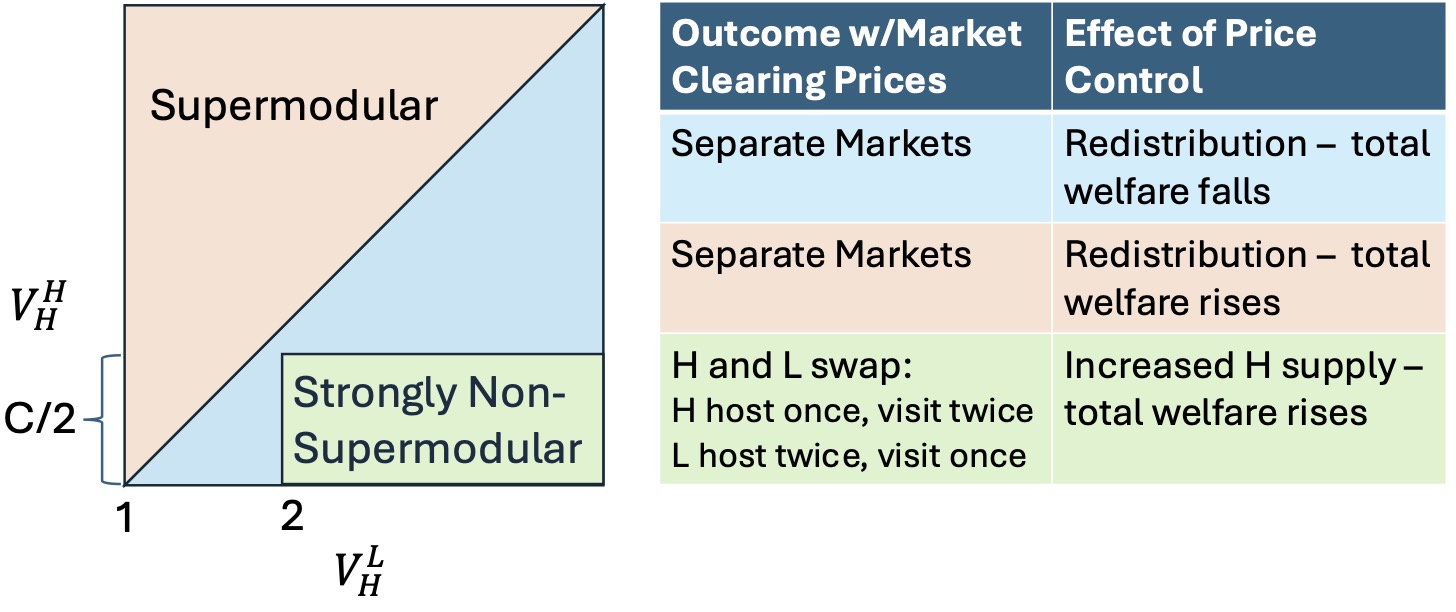

The paper describes the regimes slightly differently. The “supermodular” region is where \(V_H^H > V_H^L\) (shown in red in Figure 2), the “strongly non-supermodular region” is where \(V_H^L > 2\) and \(V_H^H < 1+C/2\) (shown in Green), and the remaining “non-supermodular but not strongly non-supermodular” region is shown in blue. (Try saying that five times out loud.)

Figure 2: Summary of Proposition 3. Price controls always hurt \(H\) types and help \(L\) types; their effect on total welfare is ambiguous. In the green regime, price controls increase supply of \(H\) type homes.

Now suppose the platform imposes price controls, requiring that prices for all homes are identical. In this case, there will be excess demand for \(H\) homes. The paper assumes that this demand is rationed randomly. When you search for an \(H\) home, half the time you succeed and half the time you can’t fine one and are forced to book an \(L\) home instead. In this case, everyone hosts twice and visits twice: on average, each person visits one \(H\) home and one \(L\) home.

This change has several effects.

- \(H\) agents are denied the opportunity to stay in two \(H\) homes (due to rationing), and also denied the opportunity to make two stays while hosting only once (due to the imposition of identical prices). As a result, this reform always hurts \(H\) agents.

- \(L\) agents suddenly have the opportunity to stay in one \(L\) home and one \(H\) home, which was not previously available to them. They always prefer this outcome to the market-clearing price equilibrium.

Thus, we already see one possible motivation for price controls: they essentially serve to transfer utility from the “rich” (those with \(H\) homes) to the “poor” (those with \(L\) homes). The effect on total welfare can go either way, depending on which group has a stronger relative preference for \(H\) homes. More precisely, in the supermodular region, price controls lower total welfare, while in the non-supermodular region, they raise it. (While I follow the math behind this conclusion, I think it should be taken with a grain of salt. As mentioned above, rescaling utilities for one type by a constant leaves their behavior unchanged, so it should only be possible to identify utilities up to a multiplicative factor. As a result, it is not clear that adding utilities across people is a meaningful way to calculate “total welfare.”)

However, the most interesting effect arises in the “strongly non-supermodular” region where \(H\) types were only renting their house out once. In this case, the price controls don’t merely redistribute visits that were already happening, they actually create more stays! The reason is that if \(H\) types want to make two visits, they now have to host twice. While this lowers the utility of \(H\) types, it offers clear benefits to the platform. (In the model it always raises aggregate welfare, though the caveat from the previous paragraph still applies).

Discussion

The model in this paper is very stylized, but I thought it offered clear intuition.

This intuition, in turn, helped me think about other markets. For example, there are competing theories about how changes to wages should affect hours worked. On the one hand, if my reward for working rises, it seems I have more incentive to work. On the other, the wealthier I become, the less I value additional money. To take one extreme, suppose I simply wish to earn enough money to live. Then increases to my wage will cause me to work fewer hours, as I can earn the money I need more quickly.

Economists call these considerations “substitution effects” and the “income effects”, respectively. While both effects seem plausible, income effects seem quite relevant in the context of home exchange platforms. Platform credits only have one use – to book homes through the platform. Furthermore, people may be reluctant to accumulate too many credits, which become worthless if the platform collapses. Therefore, it seems plausible that people with many credits accrued will decide that they don’t need to host for a while. In comparison, real money has lots of uses, so it’s harder to get to a point where more money isn’t helpful.

One important caveat is that the analysis in the paper assumes that all agents will participate in the platform. That is, agents do not have an “outside option”. In the model, controling price dispersion always hurts owners of high-quality homes (relative to simply letting markets clear). Thus, one might be worried that it could cause some of these owners to abandon the platform all together!

In practice, this might work as follows. Owners of high quality homes choose instead to rent on Airbnb. Their homes get a high price, which allows them to pay for their own trips (also on Airbnb) and still pocket some extra cash. They seem to come out strictly ahead! Why wouldn’t they do this?

The authors discuss this in the paper, and essentially conclude that several factors could be causing platform users to avoid Airbnb. For example, perhaps guests from home exchange platforms are more respectful of the property (either because of greater empathy for what it means to host, or because the types of people who are least respectful of rental properties do not tend to be property owners themselves). Alternatively, guests on exchange platforms may be less likely to expect hotel-level standards than guests on Airbnb.

These hypotheses seem plausible, but they don’t explain why these users don’t go to another exchange platform that offers market-clearing prices. That is, even if a monopolist platform might find it beneficial to constrain prices, in the presence of platform competition, platforms that use market-clearing prices might attract more desirable properties. This could create an outcome where markets for different types property are essentially separated. From a quick scan, it seems this might be happening – Trade to Travel (which sets credit prices based on estimated rental value in dollars) bills itself as a place to find luxury properties, whereas People Like Us (which uses Globes exchanged one-to-one) seems to include more “standard” homes.

The authors also briefly discuss other settings where fake money is (or could be) used. For example, some business schools use bidding systems with fake money to match students to classes, and Feeding America uses a fake money system to allocate food donations to food banks. However, as they point out, a key difference between home exchange and these systems is that in those settings, supply of goods is exogenous and agent budgets are set by the organization running the exchange. This means that there is much less potential to increase supply by constraining prices of popular goods.